Last Summer, we wrote about the upcoming opportunity for many financial institutions to recycle legacy assets into higher-coupon loans and investments. With that framework in mind, we thought it would be timely to break down the key contributors to overall earning asset yield, as yield drives margin. At HUB | Taylor Advisors, we talk frequently about the importance of mix, selection, and pricing on both sides of the balance sheet. This article will focus on the asset side of the balance sheet, given the continued runway for asset cash flow repricing.

1. MIX

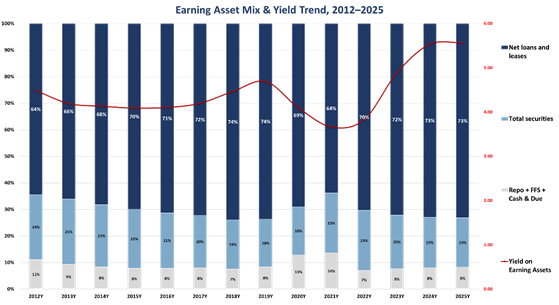

Intentionally listed first, the asset mix is generally the largest contributor to overall earning asset yields. The mix is as simple as the asset allocation: loans, investments, and cash. Despite sounding rather elementary, many factors contribute to each institution’s unique asset mix, including geography, market area, competition, credit risk tolerance, and other important ALCO risk factors. Given that most financial institutions accept the bulk of financial risk within the loan portfolio, higher allocations to loans over investments and cash largely translates to a higher overall earning asset yield. As an added benefit, lending creates opportunities for related deposits, which can and should provide margin benefit. The chart below illustrates the breakdown of the earning asset mix through time for all banks under $10B. As we can see, when liquidity builds, and the share of loans on the balance sheet shrinks, earning asset yield compresses as the balance sheet shifts towards a suboptimal mix.

Source: FDIC Call Report Data as of 12/31/2025

2. SELECTION

Once the target mix is established, selection becomes the next critical lever. Not all loans are created equal from a yield and structure perspective, and the same is true for investments. Within the loan portfolio, selection involves evaluating risk-return tradeoffs across product types: commercial real estate, commercial & industrial, residential, construction, and consumer lending all carry different yield profiles, duration characteristics, optionality, and risk weights. Additionally, the selection within the loan portfolio can have an outsized impact on the mix, selection, and pricing within a bank’s liabilities. Non-owner-occupied CRE, construction, and participation loans are generally not deposit-rich lending verticals.

Selection extends to the investment portfolio as well. The decision among agency MBS, municipal bonds, US Treasuries, or alternative sectors has meaningful implications for yield, duration, liquidity, and pledgeability, all of which contribute to net interest margin and risk management.

Importantly, selection also considers the repricing, maturity, amortization and cash flow nature of a particular asset, which is an integral part for charting the path for earning asset yields through various interest rate cycles.

3. PRICING

Pricing is the most visible lever and often the most contested. Financial institutions routinely face competitive pressures to match or undercut competitors’ pricing, and, oftentimes, pricing discussions can dominate an ALCO meeting. While a disciplined approach to pricing is important, mix and selection should largely be prioritized. Institutions should keep in mind that pricing can be flexible and should be reflective of each institution’s unique risk profile, balance sheet mix, and balance sheet selection. Two important concepts related to pricing include:

- How else can we get compensated for a loan beyond just yield? Origination fees? New deposit relationship or larger deposit balances? Treasury management services? Call protection via prepayment penalties? All of these ancillary items add value to lending beyond just yield.

- Typical bank investment products have very transparent markets. Why give up yield via paying unnecessarily higher bond prices due to excessive broker markups? Sometimes, excessive markups can translate to 10-30bps of annual yield give up.

HUB | Taylor Advisor’s Take:

The liability side of the net interest margin demanded outsized attention for the better part of the last three years. That urgency is fading. Institutions that outperform will be those that turn focus to assets with equal intensity. Mix, selection, and pricing work in concert, but have a hierarchy. An institution can have the right mix but still lose yield due to poor selection/structure. It can have the right selection but deliver lower yields due to improper pricing, leading to a suboptimal mix. A strong ALCO should consistently evaluate the mix, selection, and pricing within the asset base. The decisions made today will impact earning asset yields for years to come. The window is still open…make it count!

You have already subscribed to distributions. Thank you for your interest in our publications!